|

| |

UNIC CONCERIE ITALIANE |

& |

Assopellettieri - (Italian Leather Industry Association) |

| |

Headlines |

| |

| MIPEL128 Milan-Rho Exhibition Center September 7-9, 2025 - 1 |

| MIPEL Factory - 2 |

| MIPEL Exhibitors Spotlight - 3 |

| MIPEL Mirta - 4 |

| MIPEL 126 is waiting for you - 5 |

| MIPEL 125 - Welcome Onboard - 6 |

| Reaching and Visiting MIPEL 125 - 7 |

| The Italian leather goods sector First Half of 2021 - 8 |

| MIPEL LAB makes its debut at Lineapelle - 9 |

| THE ITALIAN LEATHER GOODS SECTOR 2020 - 10 |

| Financial support and digitalization Assopellettieri solutions to support the Italian leather goods sector - 11 |

| |

| |

|

|

| |

|

|

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy |

MIPEL128 Milan-Rho Exhibition Center September 7-9, 2025

|

MIPEL 128: the most important international event dedicated to leather goods and fashion accessories returns to Milan

from

September 7 to 9.

A special edition that brings forward the dates in view of the 2026 Winter Olympics Three days dedicated to the SS 2026 bag and accessories collections

|

|

Milan, August 29, 2025 – From September 7 to 9, 2025, MIPEL returns to Pavilions 1 and 3 of Fiera Milano-Rho, in conjunction with MICAM Milano. Now in its 128th edition, the event is exceptionally bringing forward its dates, breaking with the traditional overlap with other fashion system trade shows (Milano Fashion&Jewels, Lineapelle, and TheOne Milano). This extraordinary decision was made necessary by the work that will be carried out on the exhibition center in preparation for the 2026 Winter Olympics. This change of course, dictated by exceptional circumstances, only affects this September's edition; from the next edition (February 22-24, 2026), the show will return to its usual calendar.

Promoted and organized by Assopellettieri with the support of the Ministry of Foreign Affairs and International Cooperation (MAECI) and ITA - Italian Trade Agency, and with the patronage of the Municipality of Milan, the event confirms its status as the international benchmark for the leather goods and fashion accessories sector.

With over 60 years of history, MIPEL represents a crossroads of trends, inspiration, and business opportunities, with a highly qualified audience and over 200 brands presenting their spring-summer 2026 collections, including both historic names and emerging realities, equally divided between Italian and international brands. To further support the event and offer greater business opportunities to exhibiting companies, this edition of MIPEL will once again be able to count on the support of ITA - Italian Trade Agency through dedicated communication activities and, in particular, the international buyers incoming project. Thanks to this initiative, 23 selected professional operators from 10 countries will take part in the fair, helping to strengthen its international dimension.

Alongside the wide range of exhibits, the fair will be enriched by special projects and areas designed to promote the sector and offer visitors an immersive experience that combines tradition, innovation, and entertainment. Among the various initiatives, the Drink & Deals events are back, informal networking opportunities with the aim of encouraging the exchange of ideas and business opportunities in a convivial atmosphere. The events will be enlivened by DJ sets, tasty popcorn, and personalized Linea Daria canned cocktails—the creative studio that has made irreverent communication its trademark—to make the visit even more dynamic and engaging.

After the huge success of the February edition, MIPEL Factory returns to the spotlight in Pavilion 3 as a true interactive workshop, where artisan excellence dialogues with the most advanced technological innovations. Created in collaboration with Arsutoria and some of the leading companies in leather goods technology and supplies, MIPEL Factory offers visitors an immersive experience: they can watch live demonstrations of some of the stages involved in the creation of small leather goods items, made using the latest generation of machinery equipped with automatic vision systems and artificial intelligence. In addition, visitors will be able to personalize an exclusive leather accessory with the MIPEL logo and their initials, taking home a truly unique and unrepeatable souvenir.

Among the confirmations for the next edition—again in Pavilion 3—will be the Trend Area, which will offer an overview of the key trends for the SS2026 season through a selection of bags and accessories that fully represent their essence.

The Italian Startup Project is also back, an initiative created in collaboration with ITA – Italian Trade Agency and the Ministry of Foreign Affairs and International Cooperation (MAECI), which focus the attention on a selection of promising young Italian brands that have distinguished themselves for their creativity, contemporary vision, and ability to create products that meet market needs.

Finally, Showcase Milano, the space where design meets research and craftsmanship blends with innovation, will once again be on the spotlight with a selection of fashion and design companies chosen for their creative approach and strong stylistic identity.

MIPEL continues to strengthen its global positioning thanks to a series of initiatives that combine the physical and digital worlds. MIPEL Livestreaming, the live shopping format that sees international streamers presenting and selling products from a selection of brands at the fair live on their social media channels, has been confirmed for the September edition. This is aimed in particular at Asian markets, where this method is already very widespread and offers exhibitors an important opportunity for visibility and business.

The international vocation of the event is also expressed through its partnership with VIAMADEINITALY, the digital platform that connects over 24,000 buyers with Italian manufacturers of excellence. Thanks to this collaboration, Italian companies at MIPEL can benefit from an exclusive showcase and cutting-edge digital tools. This concrete support amplifies opportunities for contact and promotes internationalization and digitalization.

Finally, another sign of openness to the world comes from The Eastern Edge, the area inside Pavilion 3 and a section of Pavilion 5 dedicated to companies from emerging markets such as India, China, and Pakistan, which, together with exhibitors from over 18 countries, contribute to making the fair a privileged observatory on global trends and developments in the sector.

"MIPEL is a strategic moment for the entire leather goods supply chain. In a complex phase for the sector, it is essential to maintain solid reference points and continue to create spaces for openness, discussion, and business opportunities, especially in support of the small and medium-sized enterprises that form the backbone of the sector. The event remains an essential opportunity to showcase craftsmanship, support innovation, and promote the competitiveness of our companies on international markets," says Claudia Sequi, MIPEL and ASSOPELLETTIERI President.

|

| Received 01.09.25 Published 02.09.25 |

|

| |

|

| |

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy (Z1760) 20.02.25)

|

|

|

|

|

| |

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy (Z1747) 07.02.25

|

|

|

| |

|

| |

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy (Z1718) 04.09.24

|

|

|

| |

|

| |

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy

|

|

|

| |

|

| |

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy (Z1707)-1 16.02.24

|

MIPEL125

Fiera Milano-Rho

February 18-21, 2024

|

|

|

"TAKES OFF" MIPEL 125,

THE MOST IMPORTANT INTERNATIONAL EVENT DEDICATED

TO LEATHER GOODS AND FASHION ACCESSORIES WITH A NEW SECTION

RESERVED FOR TRAVEL & BUSINESS

|

- Special Showcase Milano area curated by Mirta reconfirmed.

- Revamped TREND area and exclusive performances for visitors and exhibitors.

|

From February 18 to 21 in the exhibition area of Fiera Milano-Rho, the MIPEL show returns with its 125th edition, organized with the support of the Ministry of Foreign Affairs and International Cooperation (MAECI) and Italian Trade Ageny, as the patronage of the City of Milan.

The opening of the event, along with the concurrent Micam, TheOne Milano, Milano Fashion&Jewels and Lineapelle is scheduled for Sunday 18 at 10:30 a.m. in the presence of Minister of Made in Italy Adolfo Urso.

With an itinerary of more than 4,000 square meters and 200 brands selected from historical brands and emerging companies from Italy and abroad, MIPEL will once again offer̀ a comprehensive view of the new handbags and leather accessories collections for the FW2024-25 season inside Halls 1 and 3, with an additional area dedicated to overseas companies in Hall 7.

"The Journey" is the key theme chosen for the 125th edition. From the layout to the creative concept, infact, the spaces of the event will evoke one of the symbolic places of contemporary travel: the airport, experienced not as a simple transit destination, but as a real place where the adventure begins.

The theme also fits perfectly with MIPEL's decision to expand its offerings by presenting a new area completely dedicated to the TRAVEL&BUSINESS sector: an exclusive space reserved for national and international brands that offer their collections of suitcases, trolleys, travel bags, backpacks, accessories, office bags and everything that can help make a leisure trip easier and more enjoyable, but also an away trip or a work day. Among the brands featured: Aleon, Bric's, Echolac, Got Bag, Heys, Momodesign, Plein Sport, Porsche Design, Spalding, Swissbrand, Titan, Travelite, Tucano.

|

|

Assopellettieri and MIPEL President Claudia Sequi comments, "MIPEL125 marks an important step forward in our ongoing commitment to offer a stage of excellence for the leather goods sector. With the new project dedicated to TRAVEL&BUSINESS, we aim to expand and diversify the offer presentat the fair with the goal of meeting the needs of an increasingly attentive and dynamic public. For buyers and companies, especially those of small and medium size, the show continues to represent an unmissable business opportunity to gain international visibility, as well as to compare and update on new and emerging market trends. What we propose at MIPEL is a real journey into the best of Italian and international leather goods, a theme we have precisely chosen for this edition."

After the success of the September edition, the Showcase Milano area curated by Mirta, the digital showroom that connects local contemporary brands with international curators, also returns inside Hall 1. Innovation, creativity, attention to market demands and research in the use of materials and shapes, production and processing techniques are some of the characteristics that distinguish the fashion and design companies featured in this special section.

Totally renovated inside Hall 3 is the TREND Area, the place to discover and explore the fashion trends of bags and accessories for the FW 2024/25 season. An area born from the collaboration with the MIPEL Fashion Committee, which for the study and development of trends in the world of leather goods for the coming season has been carried away by the intimate and personal history of consumers, tastes and desires that change like the surrounding reality. In this edition, the product becomes the star of this area as a representative medium of the season's themes. A selection of bags, backpacks, trolleys, gloves, hats and small leather accessories from some of the exhibitors at the fair will showcase the essential features of the FW 2024/25 moods. The area will be set up thanks to the contribution of products by: Arcadia, Biagini, Boldrini Selleria, Bruno Carlo, Caterina Bertini, Claudia Firenze, Fontanelli By Reco's, Gt Handmade, Heys, I Medici - Firenze, Keddo, Lanzetti, Marini Silvano, Minobossi Firenze, Parise, Ripani, Roberta Gandolfi, San Marco, Spalding, Tucano, Valentino Orlandi, Visonà Italia 1959.

As in the best trips, there will also be a lot of entertainment and sharing moments. Animating the days of the event will be a series of performances aimed at offering a well-rounded experience to visitors and exhibitors. It starts on Sunday afternoon, Feb. 18, with Andrea Paris - magician, comedian and illusionist made famous by successful shows suchas TúsíQueVales 2020, Italia's Got Talent 2019 and Zelig - who will entertain the audience in the afternoon with traveling performances as well as during the exclusive networking event MIPEL COCKTAIL PARTY (from 6:30 p.m. at the Trend Area) with his show "ApparisScomparis"; the evening will be rounded out by deejay sets with a pass-through dinner and open bar.

The entertainment will continue in the following days with the extraordinary company of dancers, athletes and acrobats Kataklò and the energetic funk and hip-hop dance artists Fresh'n'Clean. From Hall 1 to the TREND Area in Hall 3, the companies will give life to touring performances also involving the fashion proposals of some of the exhibiting brands (including Anneke, Boldrini Selleria, Bric's, Chiarugi, Claudia Firenze, Lanzetti, Lo Stile srl, Momodesign, Salvatore Sorrentino, Tucano, Valentino Orlandi, Visonà Italia 1959), to leave visitors and exhibitors with a baggage of emotions, knowledge and exciting experiences just like those related to an unforgettable trip.

|

|

| |

|

| |

MIPEL, the most important international leather goods and fashion accessories show - Milan Italy (Z1694)-1 22.01.24

|

Reaching MIPEL125 has never been easier: discover MIPEL hospitality services!

|

|

|

| |

|

| |

Assopellettieri - (Italian Leather Industry Association) (Z1533) 20.09.2021-1 |

| |

|

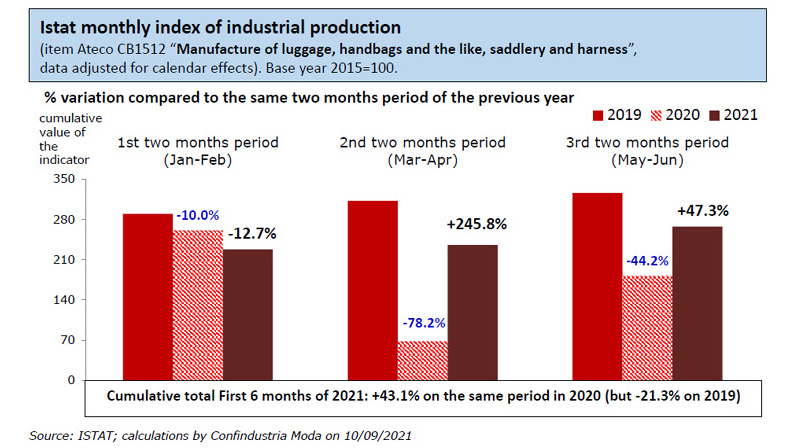

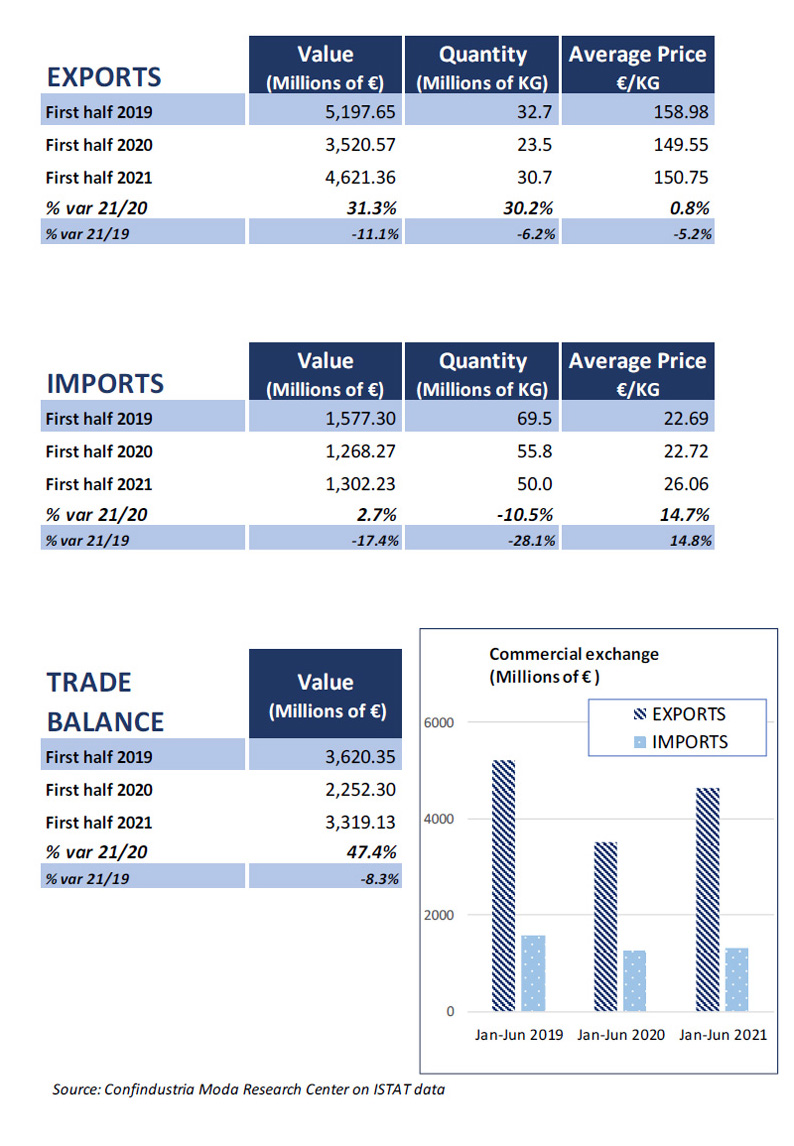

SECTOR PERFORMANCE IN THE FIRST 6 MONTHS OF 2021

Leather goods at the moment of truth: rebound or start of a solid recovery? The data of the first half of the year show significant recoveries on 2020 for all indicators: +43.1% for industrial production, +31.3% for exports in value driven by the luxury multinationals, +22.9% for retail sales on the domestic market, +29.5% for the turnover of the members reached by the survey of the Centro Studi di Confindustria Moda.

Just as in March, the comparison with the months of the lockdown - in which the sector had suffered very heavy downturns - favoured the achievement of considerable increases in the second quarter. With the sole exception of exports, however, which show a gap with the first 6 months of 2019 contained in a -11% in value (and -6.2% in KG), the other variables show gaps close to or greater than -20% on two years ago. The second half of the year will be decisive for a return to normality in a reasonably short time.

The recovery, however, has so far been patchy and multi-speed: if the luxury brands have recorded significant performances, thanks to which they have exceeded in several cases the pre-Covid levels, for the majority of companies the inevitable comparison with the situation before the pandemic still indicates significant gaps to be bridged: for 6 out of 10 companies the current revenues are "much lower" than in the first half of 2019.

Leather goods, like the other sectors of the Fashion System that were hard hit by the health emergency - which severely limited for months the occasions of use and the tourist flows, with the relevant purchases - after the annus horribilis 2020 has restarted; first of all, in a context of strengthening of world trade, with exports: among the top 10 destination markets - which in the period January-June 2021 all show, with the sole exception of the United Kingdom, sustained recoveries on last year - China, France and South Korea stand out, growing strongly even compared to the levels of two years ago.

On the domestic front, comforting signals come from the data of May and June, months in which the Istat index of retail trade was, albeit slightly, above 2019 values.

The effects of the pandemic on the fabric of small and medium-sized enterprises that make up the backbone of the sector are, however, serious: in the first 6 months of the year, Chamber figures show a negative balance of 157 companies, including industry and crafts, while the possible consequences on employment levels are worrying: in addition to the loss of the workforce employed in the companies that have ceased, critical issues also emerge from the sample survey on the Associates, according to which 42% of the sample companies have suffered a reduction in the number of employees compared to the 2020 final balance. A further record in the number of hours of redundancy payments authorized in the leather sector: 40.5 million (+3.8% on 2020), more than ten times (+916%) the number of hours in the first half of 2019.

The analysis of the trend of the main economic variables in the first half of the year gives similar indications: all show significant recoveries compared to the first half of 2020 (understandably, given the very low pace of activity in the months of lockdown due to the restrictions then in force), but still significant gaps compared to the pre-emergency situation.

The ISTAT index of industrial production, after the leap of the two-month period March-April (+246%) has marked in May-June, for the item "travel goods and leather goods", a +47.3% trend. So the upward trend continues, but the cumulative figure for the first 6 months (+43.1% compared to the same period in 2020) is still -21.3% lower than two years ago.

The quarterly survey conducted by Confindustria Moda revealed - for the sample of associated leather goods manufacturers - an average increase in turnover in the first 6 months of 2021 equal to +29.5% compared to last year.

Even in this case, the recovery is absolutely partial: the gap with the turnover that the panel had in the first half of 2019 is around -25%. Only 28% of respondents indicated that they had reached or exceeded the revenues of the first half of 2019; for 7 out of 10 companies, however, they were still "slightly lower" than then (12% of the sample) or "much lower" (60%).

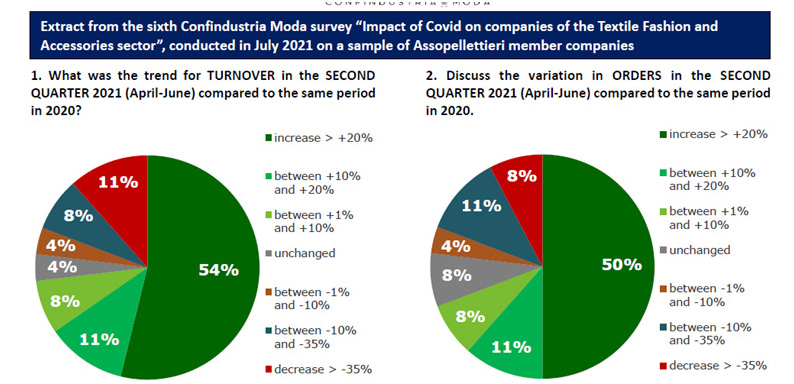

As many as 73% of the sample of Associates experienced positive dynamics in turnover in Q2 (and for 54% the increase was more than +20%), with order intake up by +28.8% in value on April-June 2020.

The recovery of revenues is destined to continue also in the 3rd quarter (as indicated by 3 entrepreneurs out of 5), even if the percentage of companies planning to resort to redundancy funds also in the third part of the year remains high (54%) (an indication of a still subdued pace in many realities). This is therefore an uneven picture.

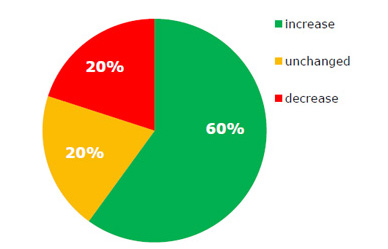

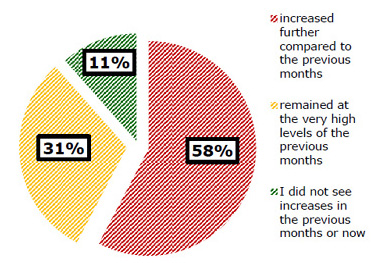

Among the critical issues that companies have to face in this phase, the tensions on the front of raw materials, whose price lists from the end of 2020 have undergone significant increases: if for 31% of operators reached by the association survey, prices in the second quarter of 2021 have remained at very high levels of previous months, according to 58% of the sample they have even increased further.

Encouraged by progress in the adherence to vaccination campaigns and the cancellation/relaxation of many restrictions (such as the reopening of shops in shopping centres at weekends in Italy from May), demand has picked up again, both at home and abroad, albeit at different rates and with some differences.

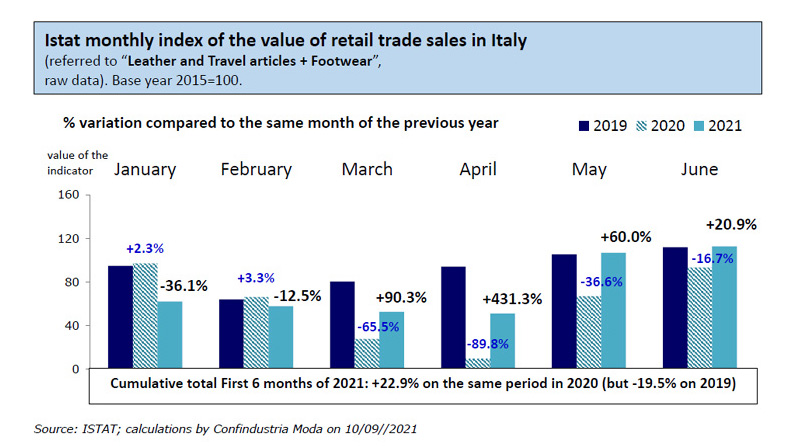

On the domestic consumption front, the Istat cumulative index for the value of Italian retail sales of footwear and leather goods in the first half of the year marks a +22.9% on January-June 2020, while remaining -19.5% below 2019 levels. Beyond the predictable surge in March and April, the most comforting data is the achievement in May and June of pre-crisis values (+1.4% and +0.7% compared to the same month in 2019): a first sign of a return to "normality", although it should be taken into account that 2019 levels were not particularly rewarding.

The problem of the lack of income from purchases by foreign tourists visiting Italy, first and foremost in the luxury segment, is of considerable importance. Although tourism in 2021 has slowly restarted (especially thanks to Europeans, traditionally not big spenders), tourism in the cities - more linked to fashion shopping - is still suffering greatly.

Even more lively the dynamics of demand from foreign markets: exports closed the first 6 months of 2021 at €4.62 billion (re-exports included), with +31.3% in value over January-June 2020, remaining however lower by -11% over the first half of 2019. In quantity (KG), recovery of +30.2% on last year; the gap with 2019 is -6.2%.

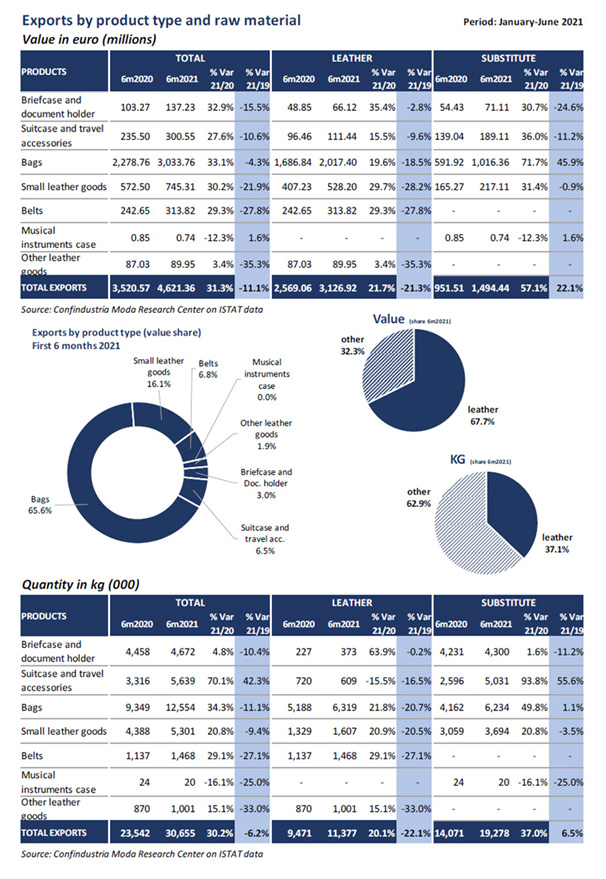

The breakdown by product type and market shows a varied situation.

An examination by commodity shows double-digit recoveries on 2020 for both leather goods (just over +20%, both in volume and value) and those made of other materials (+37% in KG and +57% in value, with excellent performances for bags). But while the latter have already exceeded 2019 levels, leather products, characteristic of Made in Italy craftsmanship, are still lower overall by -20% compared to two years earlier. Going down in detail of the items, leather bags, which cover almost 2/3 of the foreign turnover, present a +20% in value on 2020 (and a gap around -19% on 2019); belts and small leather goods (wallets, purses, key rings and pocket or handbag items) increases close to 30% in value on 2020, but at the same time gaps in the order of -28% with the pre-Covid situation.

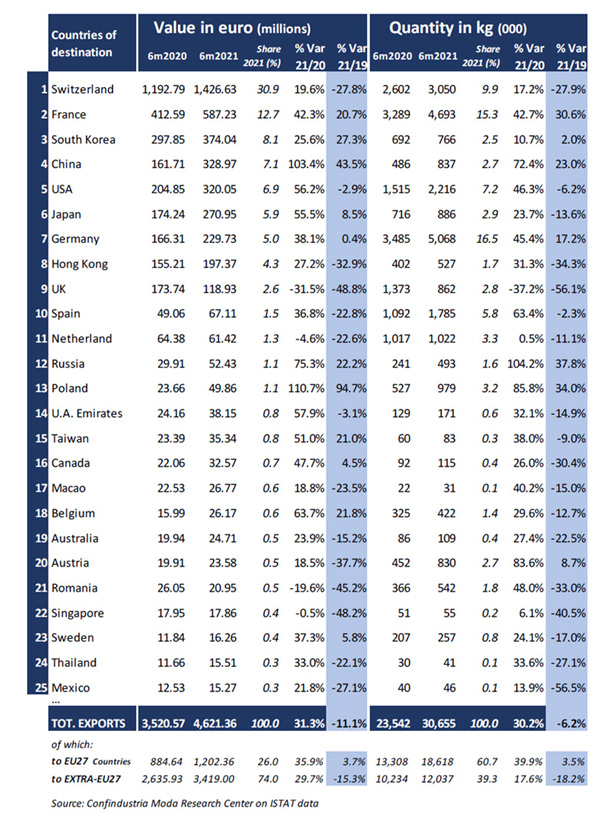

Turning to the markets, the top25 shows almost all destinations recovering in value close to, or more often than, +20% on 2020; only the United Kingdom (-31.5%), the Netherlands (-4.6%) and Romania recorded a drop after last year's setback; stable (-0.5%) was Singapore, which unfortunately had already undergone marked setbacks in the years prior to Covid.

Particularly favorable (also compared to the pre-pandemic situation) were the export trends to France (which grew by +42% in 2020 and +21% in value over 2019) - where the component of subcontracting for luxury brands is significant - China (flows doubled in value over 2020 and grew by +43.5% over 2019) and the South Korean market (increases of over 25% in value over both 2020 and 2019).

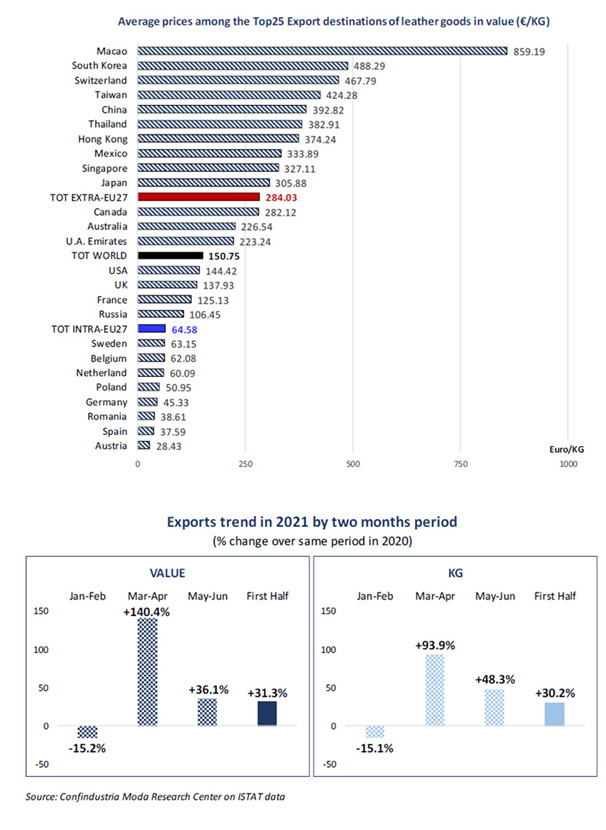

Luxury brands played a decisive role in the exploit in these two countries, the main outlets in the Far East area, as shown by the significant increases in average prices per KG (+18% on 2020 for China and +13.4% for South Korea).

The European Union partners (considered to be 27 countries, post Brexit) present, globally, a better trend compared to non-EU destinations (with increases of over 35% on 2020 in both value and KG, thanks to which they exceeded 2019 levels by +3.5%). In addition to the already mentioned France, the results in Germany (first customer by quantity) and Poland stand out.

Outside the EU (which, although increasing overall by 30% on 2020, still remains more than -15% below 2019 values), the first interesting signs of recovery are finally coming from the Russian market, which has suffered greatly in recent years, and which has exceeded January-June 2019 levels by 22% in value. The USA is also doing well - certainly facilitated by the suspension, at least temporarily, of the war of duties with the EU, which risked involving, as an American retaliation, also leather goods and other fashion sectors - and Japan: recoveries of over 55% on 2020 for both. Exports to Switzerland, the traditional logistic-distribution hub and the first destination in terms of value, while growing by +20%, remain well below 2019 values (-28%).

Incoming flows are slow: after last year's slump, imports of leather goods in the first half of 2021 show a weak +2.7% in value, with a further drop in quantities (-10.5%). China, by far the first supplier in terms of volumes (it covers almost half of them), shows a -23% drop in KG, with -8.5% in value.

The trade balance is in surplus by €3.32 billion (a recovery of +47.4% over H1 2020), although it is still -8.3% lower than in January-June 2019.

The figures for business demographics and employment are affected by the economic crisis triggered by the pandemic.

According to Infocamere-Movimprese figures, the number of active companies in Italy dropped by 157 units in the first 6 months of 2021, considering both industry and craftsmanship. For Tuscany, where almost half of the leather goods companies are based (48%), the drop was equal to -126 units; -18 the balance for Lombardy, second in the ranking. Among the first 7 regions with a leather goods vocation (which together cover almost 90% of the total number of companies), only Emilia Romagna and Veneto show positive balances compared to last December (+3 and +13 respectively).

The delays in registering cases of cessation of activity in the Chamber of Commerce database suggest that the effects of the crisis on the productive fabric will be even more evident in the figures for the months to come.

As far as employment is concerned, even though official data is still lacking, the survey conducted by Confindustria Moda highlights how, although the relative majority of the Assopellettieri members who responded (46%) declared stability in the workforce with reference to the first half of the year, the quota of companies with declining employees - in compliance with legislative constraints, given the freeze on redundancies in force - was decidedly higher (42%) than the indications of growth (12%).

Moreover, the use of wage supplementation instruments remains very high. The CIG hours authorised by INPS for companies in the leather chain (in addition to leather goods, therefore, tanneries and shoe factories) recorded a further increase in the first 6 months (+3.8%) compared to the record figures of January-June 2020 - with +2.6% for blue-collar workers (30.9 million hours) and +8.1% for white-collar workers (9.6 million) - taking them to levels ten times higher than the pre-Covid situation: 40.5 million hours authorised; they were 4 million in the first half of 2019.

Tuscany is the region with the highest number of hours granted (10.3 million, +3.1%, with 3.3 million hours in Florence and the same number in Pisa), followed by Campania (7.4 million, +45%, with Naples first in the ranking of provinces with 5 million hours, +52%), Marche (6.9 million, +13.6%) and Veneto (where the hours were reduced by 1/3, down to 5.4 million).

A result, that of the leather sector, which goes against the trend if compared to the total Italian sectors, showing a reduction of -20.3% compared to the first half of last year, mainly due to the marked decreases in the mechanical, metallurgical, chemical and wood-furnishing sectors.

In the second half of the year, 70% of associates expect a further improvement in market trends compared to the first half of the year. The next few months will be decisive for the sector to embark on the virtuous path of a sustained recovery, which will benefit not only the big luxury brands but also the many companies with their own brands, or at least small ones: if so far only 30% of member companies have stated that they have experienced the start of recovery, 62% believe that this will happen between autumn 2021 and spring 2022, obviously allowing for variants of the virus and new outbreaks.

|

|

|

|

|

|

|

Compared to the period when the lockdown was in force most companies experienced a sharp increase in turnover: indeed, 73% of the panel saw an increase in revenues compared to the second quarter 2020. For more than half of the companies (54%) this increase was greater than +20%. Nevertheless, 4% of companies had no increase on the unsatisfactory turnover levels from 2020 and 23% even experienced further reductions.

So the situation remains not homogeneous and unfortunately there are companies that still struggle to experience rewarding trends.

Considering the first 6 months of the year, by weighting responses according to company size we obtain an estimate of the average upturn in turnover for the companies in our sample of +29.5% compared to the first half of 2020; this means we are still well short of pre-pandemic levels in the first half of 2019 (about -25%). |

|

In terms of the second quarter, almost 70% of leather goods manufacturers involved in the survey reported an increase in the order backlog; for half of respondents, this increase was more than +20% in value. The percentage of companies from the sample that experienced an increase or at least stability increased to 77% (up from only 38% in the previous quarter). However, 23% of companies reported a reduction in new orders and pointed to continued difficulties in various destination markets.

Weighting responses according to company size gives us an average variation of +28.8% in the value of new orders for the sample during the second quarter.

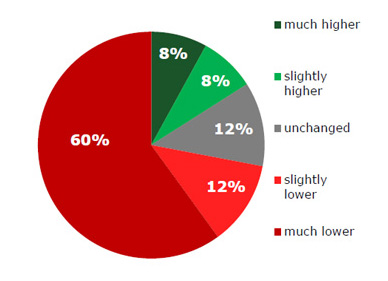

3. The TURNOVER in the FIRST 6 MONTHS of 2021 compared to pre-pandemic levels in the first half of 2019 was... |

Despite the sharp rise in the second quarter, pre-pandemic levels are still some way off: only 28% of the panel stated they had exceeded (16% of respondents), or at least equalled (12%), turnover levels for the first six months of 2019. 72% of leather goods manufacturers involved in the survey stated that they had not bridged the gap with 2019 turnover levels; while 12% of entrepreneurs reported a turnover in the first half of 2021 that was only slightly lower than pre-pandemic levels, a significant majority (60% of the sample) reported that current levels are much lower.

|

|

|

|

4. What is your TURNOVER forecast for the THIRD QUARTER 2021 (July-September) compared to the same period in 2020? |

|

5. In JUNE 2021, compared to December 2020, the WORKFORCE of your company was… |

|

|

|

46% of leather goods manufacturers reported no variation in employment levels at the end of June compared to the situation six months ago. 42% reported a reduction (as permitted by the applicable legal constraints). A significantly smaller number reported increases (12%)

6. What do you expect the WORKFORCE of your company to be in DECEMBER 2021 compared to the current level? |

|

In response to the request for a forecast at the end of the year, 54% of entrepreneurs stated they expect stability around current levels, while 35% a reduction. Few entrepreneurs expect an increase in the workforce (12%). |

|

Most of the companies in the sample (60%) expect the recovery to continue in the third quarter (most probably at a slower rate as the V-shaped recovery comes to an end or slows down). The remaining 40% is divided equally between those who expect a substantial invariance in turnover and those who instead expect a further reduction compared to 2020’s unsatisfactory levels. |

7. Does your company expect to use social security instruments (CIG wage support or similar instruments) in the THIRD QUARTER 2021 (July-September)?

|

|

|

8. Even in the Fashion supply chain a sharp increase has been reported in the price of raw materials since the end of 2020. In the SECOND QUARTER 2021 you found that these prices …

|

|

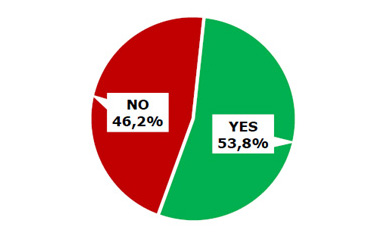

With regard to the third quarter, 53.8% of the panel expect to use social security instruments – this represents a reduction compared to the first two quarters of the year (it was close to 76% of the sample in the first quarter and 77% in the second), although the level remains high. |

|

There is no sign of respite in terms of pressure on prices of raw materials: while 31% of operators confirmed that prices had remained on par with the very high levels from previous months, 3 out of 5 leather goods manufacturers reported further increases in prices in the second quarter 2021 (58%). Only 11% of the panel did not experience any particular criticalities. |

| |

|

|

|

|

|

|

|

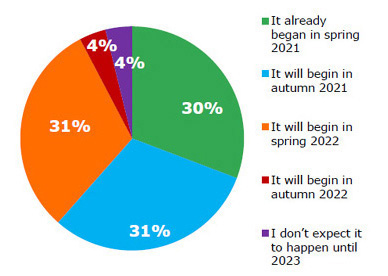

9. In your opinion, for your company the start of the recovery… |

|

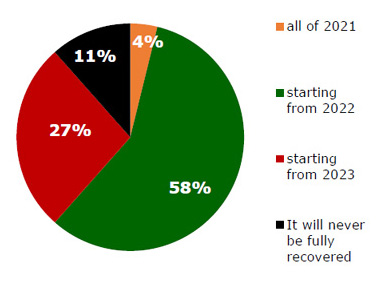

10. How long do you think it will be before you return to your pre-pandemic number of CUSTOMERS? |

|

|

|

Looking more specifically at company sentiment with regard to the evolution of the economic situation, a good 30% experienced the start of the recovery "back in spring 2021". Another 62% of the interviewees expect the recovery to occur between autumn 2021 (31%) and spring 2022 (31%). The share of those who expect even longer times is limited: autumn 2022 for 4% of respondents and "no earlier than 2023" for the remaining 4%.

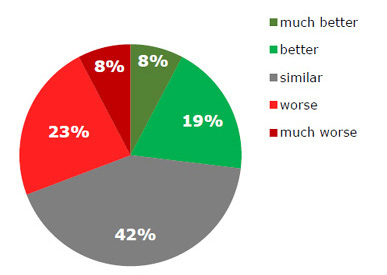

11. In your opinion, compared to your expectations at the start of the year, your company’s results in the FIRST HALF of 2021 have been… |

|

Prudence remains the prevailing sentiment even in terms of the timeframe required for returning to the pre-pandemic situation for customer portfolios: only 4% of the sample believe they will achieve this during the course of 2021. 58% expect this may occur in 2022. Compared to the previous survey there was a decrease in the number of pessimists: 27% of the panel believe they will have to wait until 2023 for a recovery; while 11% fear they will never fully get back all their customers. These two options accounted for 48% in the previous survey.

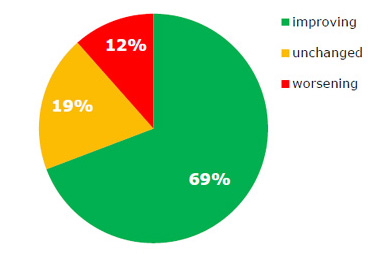

12. Compared to the first half of the year you expect the market in the SECOND HALF of 2021 to be… |

|

|

|

27% of interviewees were positively surprised by their performance in the first half of 2021; for 42% of the sample trends have been in line with their expectations at the start of the year. More than 30% of respondents were disappointed as they experienced results that were inferior to expectations (with 8% of these experiencing results that were "much worse"). |

|

We also see cautious optimism in opinions regarding market trends for the second half of 2021. 7 out of 10 operators reached by the survey expect an improvement in general demand conditions in the second half of the year; 19% think that the situation will remain unchanged; 12% of the panel fear a worsening. |

|

ITALIAN LEATHER GOODS COMMERCIAL EXCHANGE FIRST 6 MONTHS 2021

comparison with the same period of the previous yearand with the pre-pandemic levels of January-June 2019 |

|

Exports by product type and raw material Period: January-June 2021

Value in euro (millions) |

|

Exports towards the main Countries of destination

Period: January-June 2021

Ranking top 25 per value

|

|

EXPORTS

Average prices of the main destination Countries (€/KG)

Period: January-June 2021Source |

|

Imports by product type and raw material Period: January-June 2021

Value in euro (millions)

|

|

Imports from the main Countries of origin Period: January-June 2021

Ranking top 25 per value |

|

IMPORTS

Average prices of the main Countries of origin (€/KG)Period: January-June 2021 |

|

WAGE SUPPORT (CIG)

First six months of 2021 - Sector of activity: “Hides, leather and footwear”

AUTHORISED HOURS OF WAGE SUPPORT in favour of factory and office workers |

|

|

| |

|

| |

Assopellettieri - (Italian Leather Industry Association) (Z1527) 16.09.2021-2 |

22nd-24th September 2021: MIPEL Lab makes its debut

at

LINEAPELLE

|

|

|

|

|

|

|

| President of Assopellettieri Franco Gabbrielli |

|

Lineapelle CEO Fulvia Bacchi |

| |

|

|

|

Milano, 16 September 2021 - MIPEL Lab, the innovative and revolutionary project conceived by Assopellettieri, dedicated to the sourcing of Italian leather goods, makes its debut at LINEAPELLE - the world's most important exhibition for sourcing leather, materials and accessories for the fashion, luxury and design industries.

A physics, that is a new fair format in collaboration and at the same time with Lineapelle (22-24 September at pavilion 13 of Fieramilano Rho).

And a digital one, which goes beyond the 3-day presence at Lineapelle. In fact, Mipel Lab is also an "all year long" match-making platform developed by Assopellettieri in collaboration with EY and with the support of the software house DS GROUP, able to easily put the best Italian leather goods producers in contact with national and international luxury brands.

The objective of MIPEL Lab is to become the point of reference for exclusively "Made in Italy" sourcing, a link between manufacturers, brands and designers.

The President of Assopellettieri Franco Gabbrielli says: "The main objective of MIPEL Lab is to involve brands that are not present in Italy today and provide them with an innovative service to put them in contact with the most suitable producer for their needs, creating new important business alliances with national and international operators. The project meets the real need of the supply chain to join forces, because today more than ever it is essential to work as a team. Being a partner and inside LINEAPELLE is strategic, because luxury brands, designers, private labels and startups can find high profile production partners and, at the same time, discover ideal leathers and materials to create their collections. ”

This is what Lineapelle CEO Fulvia Bacchi says "We are really satisfied that Lineapelle hosts MIPEL Lab, a project that we started talking about with Assopellettieri even before the pandemic. Our fair, which has the ambition to contribute with concrete initiatives to enhance and promote the development of the entire leather industry made in Italy, is enriched and takes a further step in this direction through a high-profile synergistic operation. Italian leather goods manufacturing expresses an unparalleled quality in terms of product and service. A leadership that, by creating a system with Lineapelle's product offer and its stylistic proposal, thanks to MIPEL Lab will give rise to significant and stimulating opportunities for evolution".

MIPEL Lab is an "exclusive club" to which only Italian producers of excellence belong. The companies that will be present at MIPEL Lab during the three days of LINEAPELLE and that have firmly believed in the new project are: Bric's, Dimar Group, Mabi International, Most, Metal Studio, P&C, Pelletteria Fiorentina Montecristo, Rica, Pelletterie Sagi, Sapaf, Tigamaro, Tripel Due, Tivoli Group, to which several others will be added in the coming months.

|

|

| |

|

| |

Assopellettieri - (Italian Leather Industry Association) (Z1471) 20.03.2021-3 |

THE ITALIAN LEATHER GOODS SECTOR IN 2020

|

Short term note prepared by the study centre

|

|

The pandemic presents its bill: in 2020 industrial production and turnover will plummet, with decreases of more than 1/3 compared to the levels reached in 2019.

Exports are set to fall heavily, losing an estimated EUR 2.7 billion over the 12 months, cancelling out the strong expansion of the previous two years, while retail sales in Italy (-24.4%) have been hit hard by the restrictive measures. Despite the understandable increase in online purchases, household consumption fell significantly and tourist shopping collapsed.

Generalised, and almost always double-digit, declines in the main markets, with some positive signs (rare and weak) only in the Far East, where (despite a contraction in volume) South Korea grew in the first 11 months (+2.6%), becoming the third destination in value, and China limited its losses (-1.4%), thanks to a decisive recovery in the last months of the year.

The sector's trade balance declined by -28.6%.

For the Italian leather goods sector, therefore, no significant rebound after the spring lockdown. A decidedly poor end to the year and a still unfavourable start in 2021: after the Christmas shopping season, the new pandemic wave also hit the sales season hard, putting off the restart.

The selection among companies continues (almost 200 fewer than in 2019, between industry and handicrafts) and employment tensions emerge: 8 out of 10 companies surveyed resorted to shock absorbers in the fourth quarter. In the entire leather industry, 83 million of wage support hours were authorised in 2020 (+900% on 2019).

All the main sector variables showed markedly negative trends in 2020, with little improvement in the third and fourth quarters. In fact, the resurgence of contagions led to a further slowdown in activity in the autumn, further delaying the expected rebound, which will have to await the widespread introduction of vaccination campaigns.

-The Istat index of industrial production recorded a drop of -33.9% on January-December 2019. After the collapse of the March-April two-month lockdown and very reduced rates in May-June, the third quarter recorded contractions of around -30%. In the last part of the year, after an encouraging -3.3% in October, production activity suffered a new sharp downturn: -25% in November and -23% in December.

Similar indications come from the survey conducted by the Confindustria Moda Study Centre on a sample of companies associated with Assopellettieri, according to which only 8% of those interviewed reached or exceeded in 2020 the quantities produced in the previous year, compared to decreases of over 35% for more than half of the panel.

-The same survey also looked at how companies' turnover will develop in 2020. The distribution of responses was eloquent: for half of the sample (52%), the decrease was between -20% and -50%; and a further 24% experienced drops in revenues of even more than -50%.

Overall, the panel recorded an average drop in turnover of -36.9% in 2019, which -if applied to the entire sector -would lead to an annual loss of €3.3 billion. This would fall from €9 billion (estimated considering only companies based in Italy) to €5.7 billion. Although sample-based, this is an indication of the serious difficulties that companies have been facing since the start of the pandemic.

On the domestic front, the ISTAT index of the value of retail sales of 'Leather goods and footwear' shows, with reference to the whole of 2020, a drop of -24.4% compared to 2019, on which the two spring months of suspension of physical sales, the fewer opportunities to use goods caused by preventive measures, but also the climate of mistrust among consumers, in an economic phase characterised by great uncertainty for the future, obviously weigh heavily. Despite the understandable growth of e-commerce, therefore, Italian households' purchases in 2020 fell considerably.

After a "promising" August (-0.7% compared to the same month in 2019), in September and October domestic demand lost strength again (-8.7%), and then collapsed in November (-45.5%), when further restrictive measures were introduced to cope with the new emergency wave. Heavy repercussions were also felt in December, a crucial month for shopping for clothing and accessories for Christmas presents (-14.4%).

To make matters worse, there was also, of course, the collapse in tourist purchases, which particularly affected high-end products.

-As far as foreign demand is concerned, in the first 11 months of 2020 (latest data available to date), exports showed a significant setback, both in value (-26.2% compared to the same period in 2019) and in KG (-23.1%), abruptly putting an end to the expansive trend of recent years: leather goods were exported for 7.08 billion euros, corresponding to 46.4 million KG. The average price per KG fell by -4.1%.

Exports thus returned to just above the levels of the first 11 months of 2017, abruptly "burning" the marked increase achieved in the two-year period 2017-2019 (+40% in value). On the basis of 12-month projections, foreign sales have lost almost EUR 2.7 billion for the whole of 2020.

In KG, on the other hand, we have to go back as far as 9 years ago (2011), just after the global economic crisis, to find such a penalising trend.

As for the other variables, also for exports the trend in the last two quarters of the year was still far below expectations (-18% in value in the third quarter and -21% in October-November), bringing no significant improvement compared to the first half of the year, strongly penalised by the -61% recorded in the two-month period March-April lockdown.

All the main types of goods showed significant declines. Handbags (by far the most exported item, with a 65% incidence on the foreign turnover) show drops of -21.5% in value; suitcases around -25%; even more unsatisfactory are the trends for small leather goods (i.e. wallets, purses, key rings and pocket or handbag items, -34%) and belts (a drop of over -40%, both in value and in KG).

Looking at the items by material, on the whole, leather products -typical of Made in Italy production and representing more than 70% of the total in value terms -show heavier contractions (in the order of -30%, both in value and in KG) than those in substitutes, whose exports fell by -15.4% in value and -17% in KG.

An analysis by destination also shows that almost all markets have declined in quantity and value. There are very few exceptions: in the ranking by value, among the top 25 outlet countries, only South Korea (+2.6%), Poland (+2.3%) and Taiwan (+0.3%) show a positive sign compared to January-November 2019 (accompanied, however, by declines in KGs). Thanks to this result, South Korea (which had grown 77% in value over the previous three years) moved up to third place in the ranking, overtaking the USA (which, on the other hand, recorded declines of over 30% in both value and volume in the first 11 months of 2020). China lost only -1.4% in value, thanks to the recovery recorded in the two-month period October-November (+40.5%). No country in the top 25, on the other hand, recorded increases in KG.

There was a marked reduction (close to -38% in value) in flows to Switzerland, the leading destination for exports in value terms and for some time now the logistics-distribution platform for the major international luxury brands.

The European Union (from this year onwards considered to have 27 members, post Brexit) saw an overall decrease of 20% in value and 22% in KG. France lost almost 10% in value (with -6% in KG), another traditional destination for third-party production for designer labels, which became the top customer in terms of quantity for Italian operators, overtaking Germany (which lost 20% in value and -14% in KG).

Among the non-EU countries -which showed a heavier contraction in terms of value than the EU markets as a whole, equal to -28% -the Far East lost -13% in value and -19% in KG, with significant drops in several countries (Japan -15.5% in value, Hong Kong -31%, Macao -20%, Singapore -46%).

Russia and the United Arab Emirates also fell (-19% and -28% respectively in value), as did Canada (-21%) and the United Kingdom (-23.5%, with which the EU signed a trade and cooperation agreement, TCA, at the end of December, with immediate provisional application).

-Imports of leather goods, which amounted to 2.37 billion euros between January and November, were down by -21% in value and -25% in KG. China, the leading supplier in terms of volume with a share of close to 50% of the total, showed a decrease of -35.4% in value (-39% in KG).

-Although the trade balance remains largely in surplus, it is down 28.6% on the first 11 months of 2019: a surplus of €4.7 billion (almost €1.9 billion less). In spite of the sharp decline, this is still a significant result, which places leather goods in 6th place in terms of assets among the 99 goods chapters of the customs nomenclature (it was 5th at the end of 2019).

The delicate economic situation is likely to have serious consequences for the sector's production fabric, which has always been based on a network of small and very small enterprises.

-The selection of companies continued in 2020. Although it is too early to read in the Chamber of Commerce registers the effects that the current economic crisis will have on the demographics of companies, the Infocamere data on company births and deaths already show the first signs: at the end of 2020, they record a balance of -199 units in the number of active leather businesses compared to December 2019 (-4.4%) between industry and craft, with a significant worsening in the fourth quarter (-87 units).

Broken down by region, Tuscany (where about half of the companies are concentrated) shows a negative balance of -116 companies compared to 2019; Veneto -30; Abruzzo and Lombardy -20 and -17 respectively; 16 less in Emilia Romagna. The balance in Marche is smaller, but still in double figures (-12). Campania is bucking the trend (18 more units on end 2019). The remaining regions show a total of 6 fewer companies.

It is easy, however, to foresee a significant widespread worsening in the coming months, when the realities that have not been able to overcome the exceptional difficulties that operators have had to face as a result of the emergency, which is still ongoing, will begin to be counted.

-The first critical points have also begun to appear on the employment front. The processing carried out by the Confindustria Moda Study Centre on Chamber data shows -despite the freeze on redundancies imposed by government measures -a drop in the workforce of around -2% (an order of magnitude also reiterated by the member companies reached by the survey) following cessation of activity or as permitted by law (consensual terminations, retirements, non-renewal of fixed-term contracts...).

The same survey highlighted a strong recourse, also in the fourth Quarter, to wage supplementation tools (8 out of 10 companies in the sample), which is also confirmed by official INPS figures.

In fact, these figures show an unprecedented increase in the number of wage support hours authorised in 2020: 83 million hours for companies in the leather sector from January to December (8.3 million in 2019), an increase of +900%.

Never had such a number of hours been granted, not even in 2009 (23.1 million) or 2010 (29.7 million) at the height of the global recession.

All the main district areas of the leather industry show considerable increases: Tuscany is the first region for authorised hours (24.3 million, +3954% on 2019, of which 11.5 million for the province of Florence, +5193%), followed by Veneto (14.9 million, +934%), Marche (12.9 million, +370%), Campania (11 million, +685%) and Lombardy (+797%).

These figures testify to the exceptional reduction in activity levels during the year and the seriousness of the current situation.

-There is great concern about the situation in the coming months. The indications of the entrepreneurs, collected at the end of January, interviewed about the turnover expected in the first quarter of 2021 seem to replicate, with a very slight improvement, those expressed for the last 3 months of the year: the average drop within the sample is equal to a heavy -23.6%.

Only 3% of respondents expect a start to recovery in the first half of this year; for 52%, it will be necessary to wait until the second half of 2021; for the remaining 45%, the entire year will be characterised by an unfavourable trend. The time frame for a real recovery

conditioned by an efficient vaccination plan and a gradual return to normality still seems uncertain and in any case not immediate.

Milano, March 9th 2021

|

|

| |

|

| |

Assopellettieri - (Italian Leather Industry Association) (Z1419)-5 |

Financial support and digitalization

Assopellettieri solutions to support the Italian leather goods sector

|

|

STATI GENERALI DELLA PELLETTERIA ITALIANA |

Florence, 23 July 2020 - Aggregation, digitalization, internationalization, sustainability, credit and finance: these are the five pillars on which Assopellettieri focuses on relaunching the business. On Thursday 23rd July was held in Florence the event The States General of Italian Leather Goods Sector, organized by Assopellettieri and co-promoted with the Municipality of Florence with the aim to clarify the Italian leather goods sector situation consequently to Covid-19 emergency. Assopellettieri, since the beginning of this emergency, has fought to hear the alarm voices of the companies in the sector, a 9 billion euro supply chain (2019 data) which 85% consists of exports. The choice of Florence as the venue for this event has an important symbolic value: Tuscany represents one of the most important production districts in the world of leather goods, 60% of the Italian production comes from this region that represents one of the main economic assets.

During the morning attended Cristina Giachi Deputy Mayor of Florence, Franco Gabbrielli Assopellettieri President, Manlio Di Stefano Undersecretary of State for Foreign Affairs and International Cooperation, Carlo Ferro ITA-Italian Trade Agency President, Mauro Alfonso CEO Simest Spa, Eugenio Giani President of Tuscany Regional Council, Andrea Calistri Assopellettieri Vice President and Delegate for the Tuscan District, Paola Castellacci CEO Adiacent Spa, Simona Bonafè MEP.

«I would like to send a positive message, we need to react and we cannot wait: we have to strengthen our Association and work together to overcome the difficulties - said Franco Gabbrielli Assopellettieri president -. Assopellettieri has to do that, today. We invite all companies, from the smallest to the biggest one, to join us, each with its own characteristics and requests.The Association has the opportunity to discuss and interact with the Government; the funds are there and we can be the spokespersons of the companies in this step. Through the synergy with ITA-Agency, Simest and MAECI, the Association aims to offer concrete solutions for leather goods companies relaunch by providing answers to the liquidity, market and product crisis. Especially with Simest through the supply of advantageous loans and with ITA through initiatives designed to ease the internationalization process. Assopellettieri, through the Mipel digitalization and the Miss Bag initiative, is also proposed as a solution to give the opportunity to intercept markets ".

«You have a great task, making choices that will ferry this strategic sector into the future it deserves. We have an incredible patrimony that is in your hands, in your heads, in the work that you know how to inspire with your co-workers - the Deputy Mayor Cristina Giachi said at the opening, bringing greetings from the Municipality of Florence».

"Between Assopellettieri and ITA, the spirit of the system that concretizes the proposals bringing them to the end and guaranteeing their realization is stronger than ever - explained the president of ITA, Carlo Ferro -. ITA and MAECI continue to provide services useful to small and medium-sized enterprises and confirm the new editions of the September/October trade fair events in Italy. The incoming of international buyers from mainly intra-EU countries continues and gets stronger. The Silent Mipel Showroom is a new event, a post Covid version of the traditional Mipel showroom that will take place in an exhibition centre in the commercial heart of Seoul able to connect to the virtual fair and to the online commerce. Last but not least, the B2B platform that will put companies in contact with operators in foreign markets, ensuring remote meetings, autonomous exhibitions and business work ».

"The export agreement, recently signed by Minister Di Maio, is based on six specific pillars mainly declined on two concepts: strengthening Made in Italy on international markets and increasing the internationalization of the entire Italian economic district. These are communication, training, e-commerce, exhibition system, integrated promotion and subsidized finance. The latter is the beating heart of the reform: we have allocated 900 million euros, 300 of which are non-refundable. 70% of the resources are allocated for small and medium-sized enterprises - said Manlio Di Stefano Undersecretary of State for Foreign Affairs and International Cooperation».

"The international scenario is complex but has to be interpreted as an opportunity to restart and cover incremental competitive positions compared to the past - explained Mauro Alfonso CEO Simest Spa -. Our role is to facilitate companies in the process of internationalization both with direct investments abroad and with the management of state funds such as Fund 394. We have made evolutions of this tool which affects 7 fundamental measures. The first relates to the participation in fairs and exhibitions reserved for SMEs, for which the financed amount is up to a maximum of 150 thousand euros; the second proposes insertion programs on non-EU markets by financing the opening of permanent commercial structures, the maximum amount that can be financed for both SMEs and companies of any size has been raised from 2 and a half million to 4 million euro. Feasibility studies are another financeable tool as long as they are linked to foreign investments: the maximum amount is up to € 200,000 for commercial investments and € 350,000 for productive investments. We also have the opportunity to finance technical assistance programs with which we support staff training in foreign investment initiatives, up to a maximum of € 300 thousand.The temporary export manager and the temporary digital export manager are figures that can be financed with the 394 Fund, up to a maximum of 150 thousand euros. We can also contribute to e-commerce by supporting companies through the use of their own market places or platforms up to a maximum of 450 thousand euros. The last tool is the capitalization of exporting SMEs, whose maximum funding ceiling has been raised from 400 to 800 thousand euros. We are able to carry out the assignment procedures quickly and respond within 30 days, bypassing the guarantees of the credit system and being able to access a rate of 0.085%. It is also possible to use a non-repayable loan quota. In addition, we want to offer the leather sector, for participation in exhibitions and fairs and for Mipel, a series of measures including: subsidized financing up to 100% with a duration of 4 years, of which the first one is pre-amortization, at 0.085%; 50% of the costs relating to the equity investment granted without recourse; important news is that it will be possible to finance participation in international fairs that take place in Italy. Participation in fairs is therefore a commitment accessible to all operators ».

«The institutions have to provide the necessary support, because the tannery and leather goods manufacturing system have to be strongly supported. The resources that come from Europe have to be translated into projects to be carried out together; I believe it is necessary to equip a real task force in this direction in the Region. An important synergy between the Association and the Region has to be created, in order to have projects ready when the funds arrive - was the comment of the President of Tuscany Regional Council Eugenio Giani ".

"One of the assets that Assopellettieri has and no one else has is the most important leather fair in the world, Mipel, which celebrates 60 years in 2021 - said Andrea Calistri, Assopellettieri Vice President and delegate for the Tuscan District -. And in September the fair will be there, together with colleagues from Lineapelle and Micam, with a completely new model to go with Italian companies towards a potentially global market.

We have already started working on a multi-tasking platform with a totally innovative format also from the point of view of the fair's tour: making it 'open' 365 days a year thanks to the digitalization of the fair system. In addition, the Miss Bag initiative will be launched in September: an iconic bag that all leather manufacturers participating in Mipel will be called to interpret according to their own style, thus also allowing companies that do not normally develop a product to create something of their own to exhibit all over the world ».

"With a business digitalization point of view, there are three considerations to think about - said Paola Castellacci CEO Adiacent Spa -. The first is the need to put together digital channels with the offline ones in order to improve a daily dialogue; the second is e-commerce which we have seen growing fast and in this lockdown period with 2 million new customers in sectors and age groups previously absent (+ 55% compared to 2019): we have to therefore evaluate which companies can benefit from these numbers; the third theme is globalization, to be reinterpreted from a digital export perspective all over the world. Digital must truly be central starting from training, also bringing new figures working in the sector to the company».

"Urgent and massive interventions are needed to ensure the economic sustainability of a supply chain that has always been a source of pride for our country - said MEP Simona Bonafè -. We need far-reaching innovative policies and measures; we need a national and European public enormous intervention like never seen before and an extraordinary commitment of citizens and businesses. At European level has been launched the largest recovery plan in the history of the European Union: a 750 billion plan of which 390 billion in direct subsidies. Of these, 208 billion will go into strategic investments in our country: I believe that the two areas in which to invest is sustainability and digital that will affect every part of the economy, society and industry. And this will require the transition from the current linear production to the circular economy. And the leather goods district has understood this for some time."

|

|

| |

|

|

|

.jpg "DISCOVER MIPEL Factory: a special projetct for next MIPEL edition!")

.jpg "VISIT MIPEL AND DISCOVER MIPEL Factory: experience the art of leather goods in a real workshop, take a closer look at the creation of leather items and personalise your MIPEL keyring with your initials")

.jpg "BUSINESS, COCKTAIL & GOOD VIBES: take a break from business and immerse yourself in the relaxed atmosphere of ''DRINKS & DEALS'' @MIPEL Facotry!")

.jpg "WHERE & WHEN: HALL 3 - BOOTH R12 | Don't miss ''DRINKS & DEALS'' appointments")

.jpg "In collaboration with: Linea Daria & Arsutoria school")

.jpg "JOIN MIPEL - GET YOUR FREE TICKET!")

.jpg "BONFANTI: find out more!")

| FW 2025/26 COLLECTIONS")

| SS2025 COLLECTIONS | FieraMilano-Rho (Milan, Italy)")

")

|| 15/17 SEPT. - 9.30am-6.30pm (HALL 1-3-7)")

|| 15/17 SETT. 9.30-6.30 (PAD. 1-3-7)")